8 charts · 8 business insights

Each chart pairs a data observation with a KRX operational-context interpretation. (≈ 30 seconds per chart · about 5 minutes total)

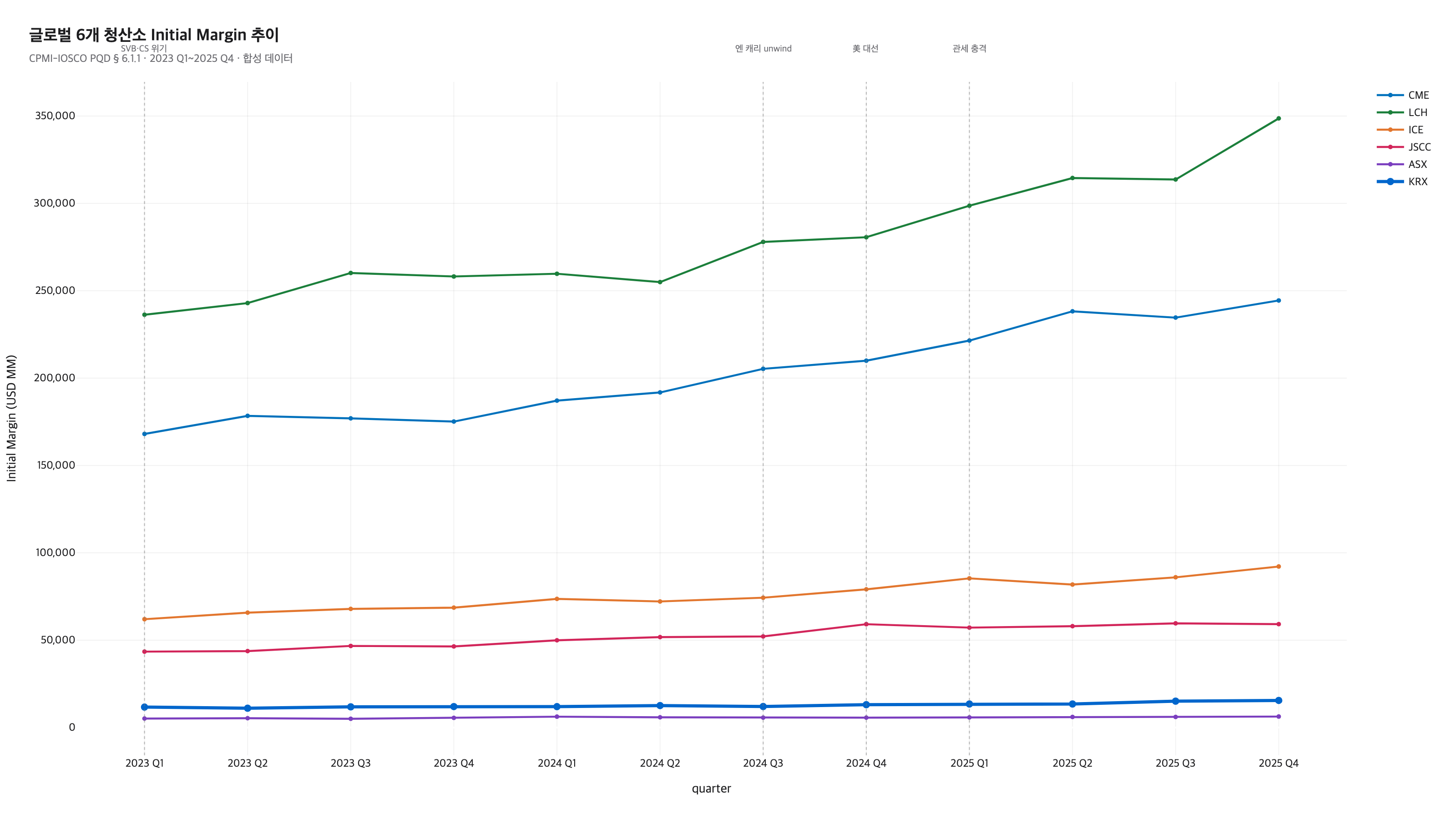

Initial Margin time-series comparison

In the 2025 Q1 tariff-shock quarter, margins rose simultaneously — ICE +7.9% · LCH +6.4% · CME +5.5% · KRX +2.9% · ASX +2.0%, a spike at 5 of 6 clearinghouses. Only JSCC was an exception at -3.3%.

Applied to KRX: Trade-policy swings such as a tariff shock affect EMEA · Americas · APAC at the same time. Member firms exposed to markets outside Korea should secure margin calls and liquidity ahead of quarters where a macro event occurs.

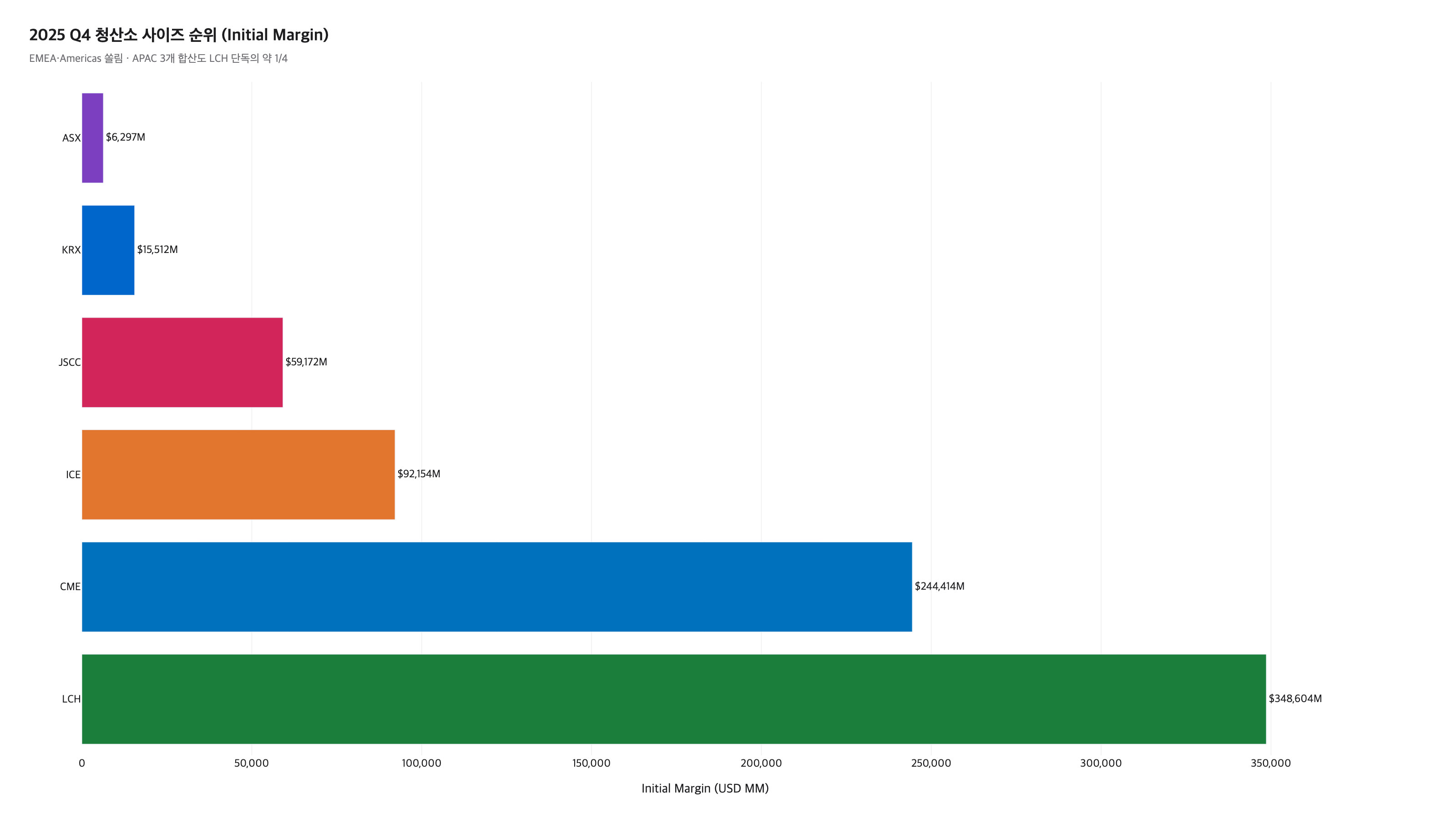

2025 Q4 clearinghouse size ranking

LCH ($349B) > CME ($244B) > ICE ($92B) > JSCC ($59B) > KRX ($16B) > ASX ($6B). EMEA (LCH alone) > Americas (CME+ICE = $336B) > APAC 3 combined ($81B) — a clear concentration in EMEA · Americas. Even the APAC total is roughly one quarter of LCH alone.

Regional comparison: Global clearing infrastructure is concentrated in EMEA · Americas. The APAC trio combined is still about one quarter the size of LCH alone — to anchor KRX operational decisions on top of this size gap, information sharing among clearinghouses in the same region carries significant value.

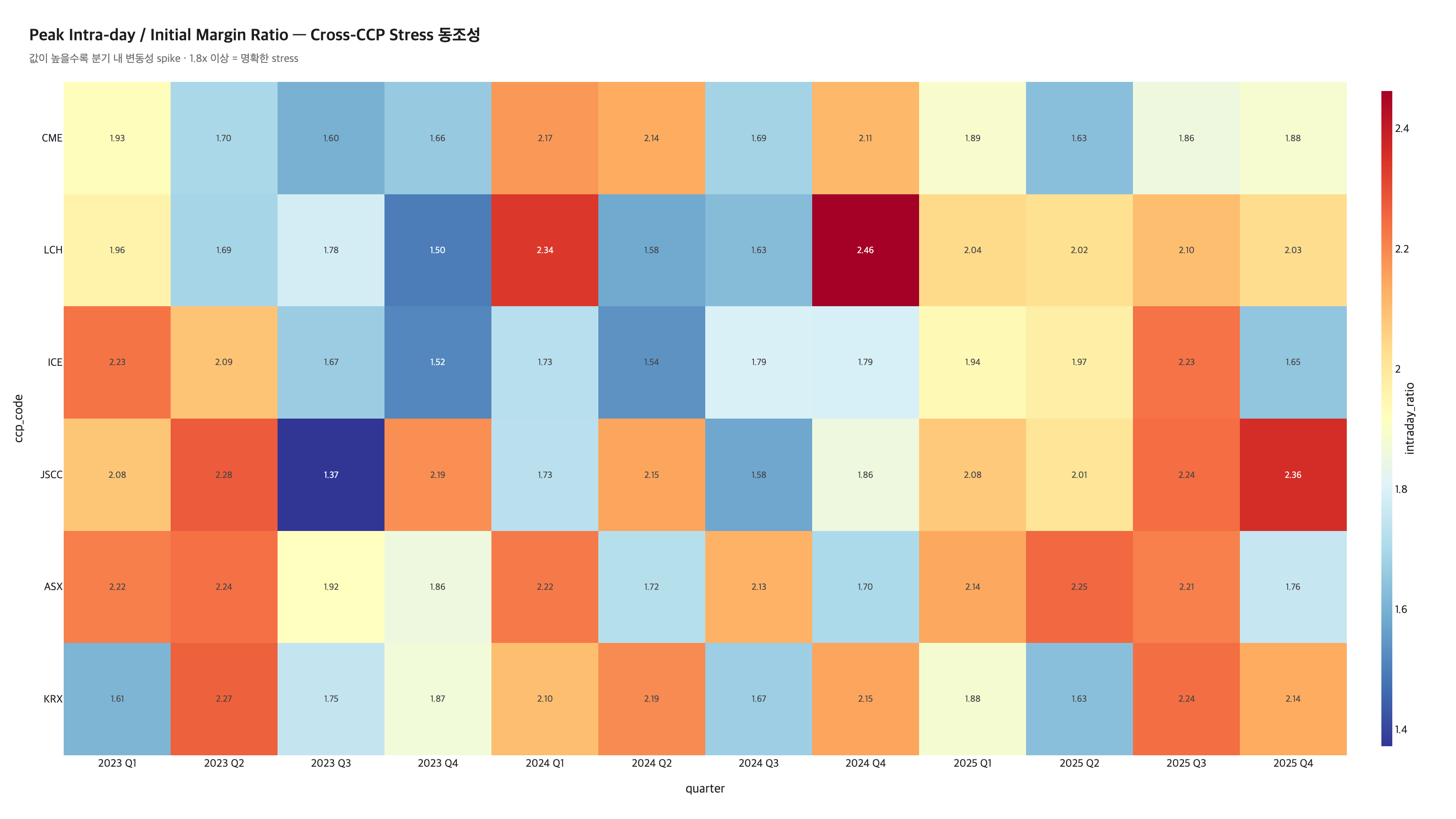

Peak Intra-day / IM Ratio heatmap (Cross-CCP stress synchronization)

In two quarters, 2025 Q1 and 2025 Q3, all 6 of 6 clearinghouses hit a ratio of 1.8x+ at once. 2023 Q1 (SVB) 5/6, 2024 Q1 (BOJ) 4/6, 2024 Q4 (US election) 4/6 show partial synchronization. Non-stress quarters stay around 1/6.

Reporting flow: Distinguishing whether a value spiked at a single clearinghouse or whether several CCPs moved together in the same quarter changes the internal reporting threshold. When a simultaneous spike is detected, it can be classified not as a single clearinghouse's transient move but as a macro-environment shift, and escalated for separate analysis and executive reporting.

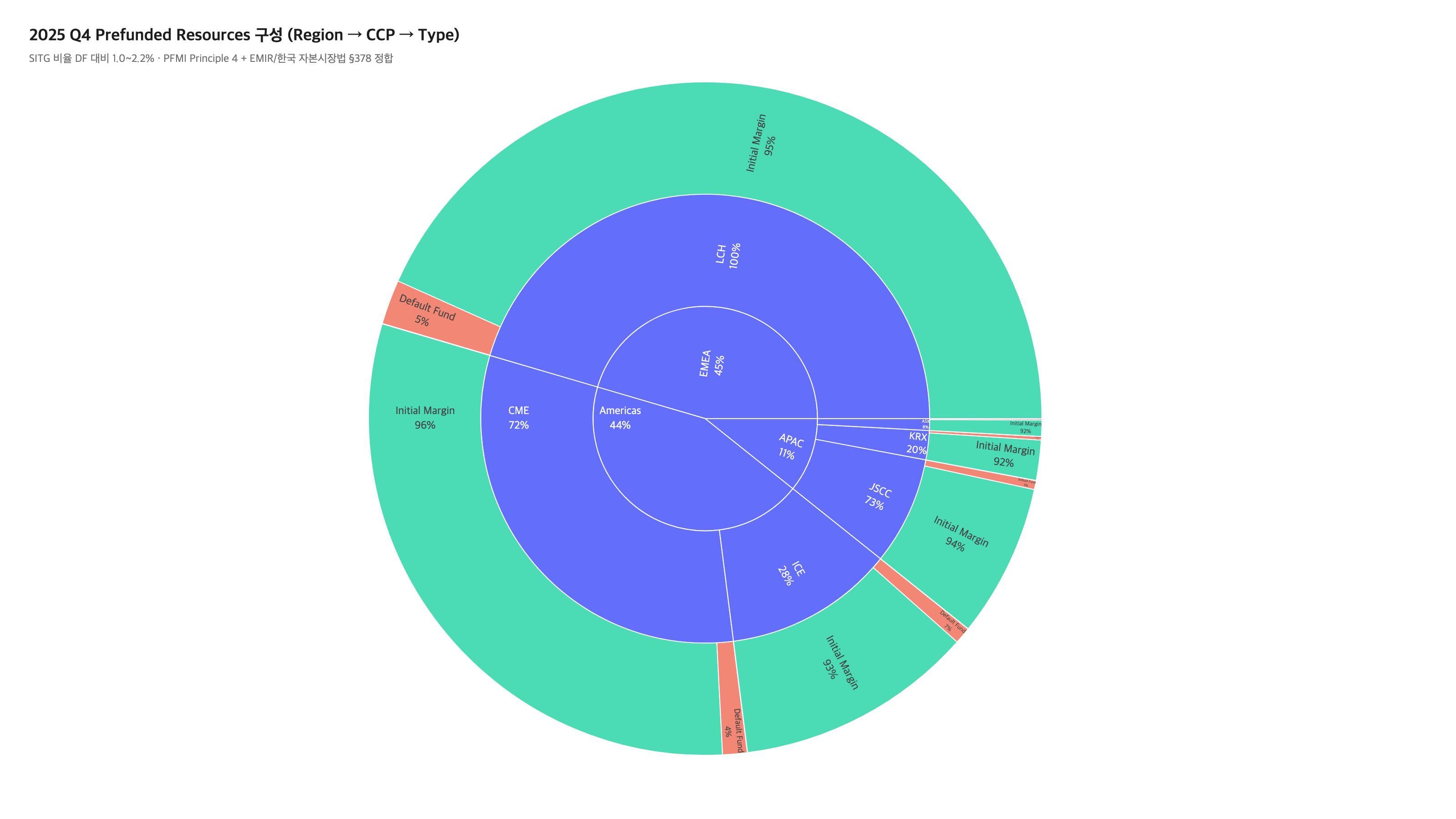

2025 Q4 Prefunded Resources composition (Sunburst)

Initial Margin accounts for 91.9–96.2% of prefunded resources (95.2% combined). Default Fund is 4–9% of IM, and SITG (skin-in-the-game) is 1.0–2.2% of the Default Fund. KRX's SITG ratio is 2.2% (vs DF) — higher than the synthetic-data average (1.6%).

Member firm briefing: This is a structure conformant to PFMI Principle 4 + CPMI-IOSCO PQD § 4.1.4 (EU CCPs additionally apply the ≥25% RTS under Commission Delegated Regulation 153/2013 Article 35 · Korea applies the Financial Investment Services and Capital Markets Act §378 + the FSC's Clearing and Settlement Business Regulation separately). SITG sits in the default waterfall after the defaulting member's own resources are exhausted first, and its position relative to the mutualised DF diverges by CCP — e.g., KRX moved SITG ahead of the mutualised DF through the 2015 amendment to the Capital Markets Act (in the wake of the 2013 HanMag incident). It serves as supporting material when explaining to member firms that the CCP is directly committing its own capital to the loss-absorption order.

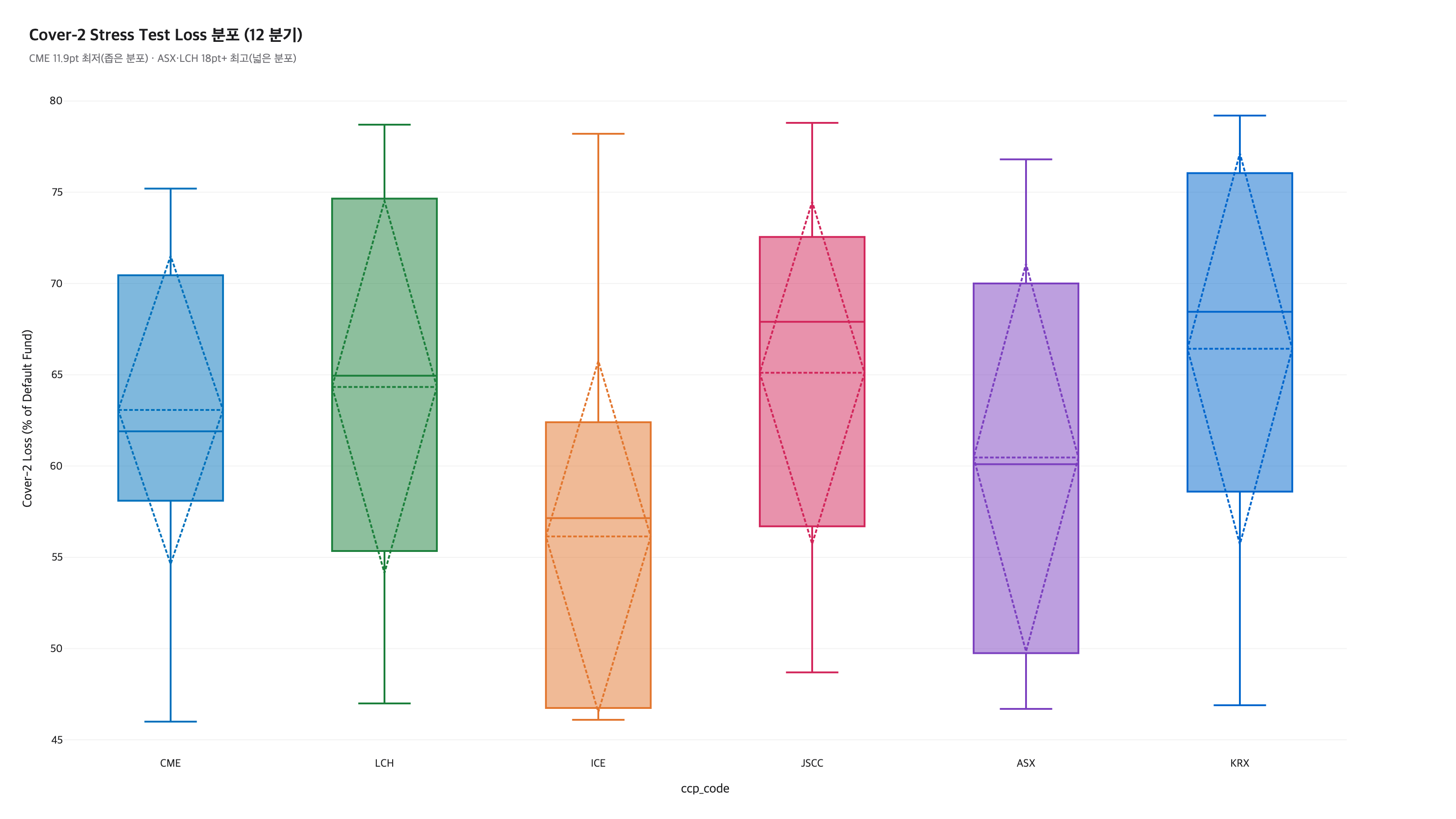

Cover-2 Stress Loss distribution (12-quarter box plot)

Cover-2 loss IQR by clearinghouse — CME lowest at 11.9pt (stable), ASX 18.5pt · LCH 18.3pt highest (volatility exposure). The APAC vs Americas/EMEA boundary is not clear-cut; it depends on each clearinghouse's asset composition.

Risk operations: Differences in cleared-asset diversity / concentration and margin-model calibration drive the variability of stress-test results. A narrow distribution signals stable model calibration; a wide one puts tail-risk response + calibration review on the next quarter's review agenda.

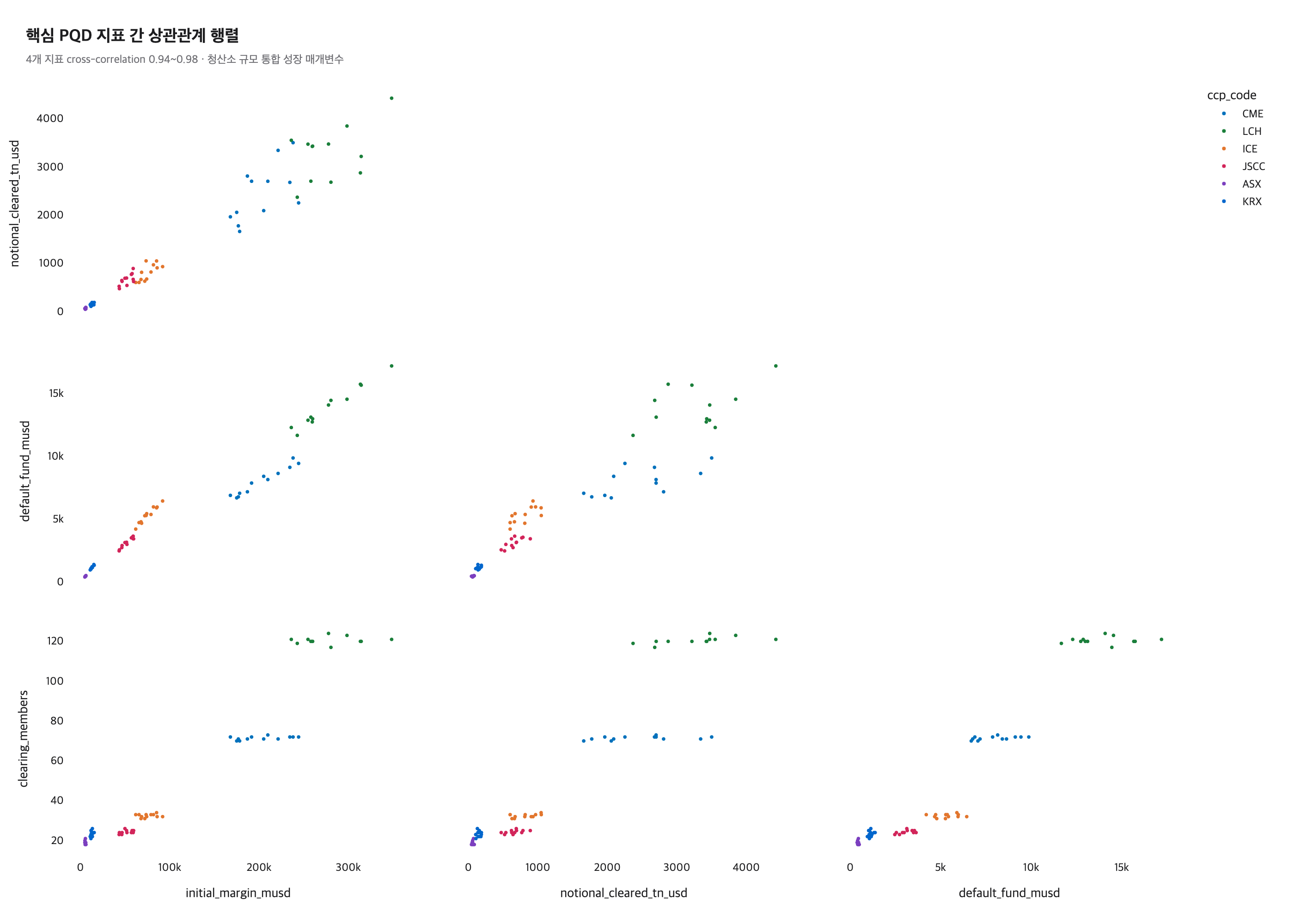

Correlation matrix across PQD metrics (Scatter Matrix)

Initial Margin is strongly correlated with all three other metrics — Default Fund 0.977, Notional Cleared 0.973, Clearing Members 0.963. Cross-correlation across the 4 core metrics is 0.94–0.98 (※ co-movement is inherent to the synthetic-data structure — a similar pattern is also observed in real PQD).

Growth tracking: Trading volume, member count, and capital scale appear not as separate metrics but as a single growth axis that moves together. When KRX introduces new products or expands the market, estimating only the change in trading volume can carry the accompanying expansion in members and capital within the same picture. (Participation in Korea's market clearing infrastructure has a separated structure: a mandatory pass-through to KRX as the sole CCP under Capital Markets Act §378 + voluntary application for membership.)

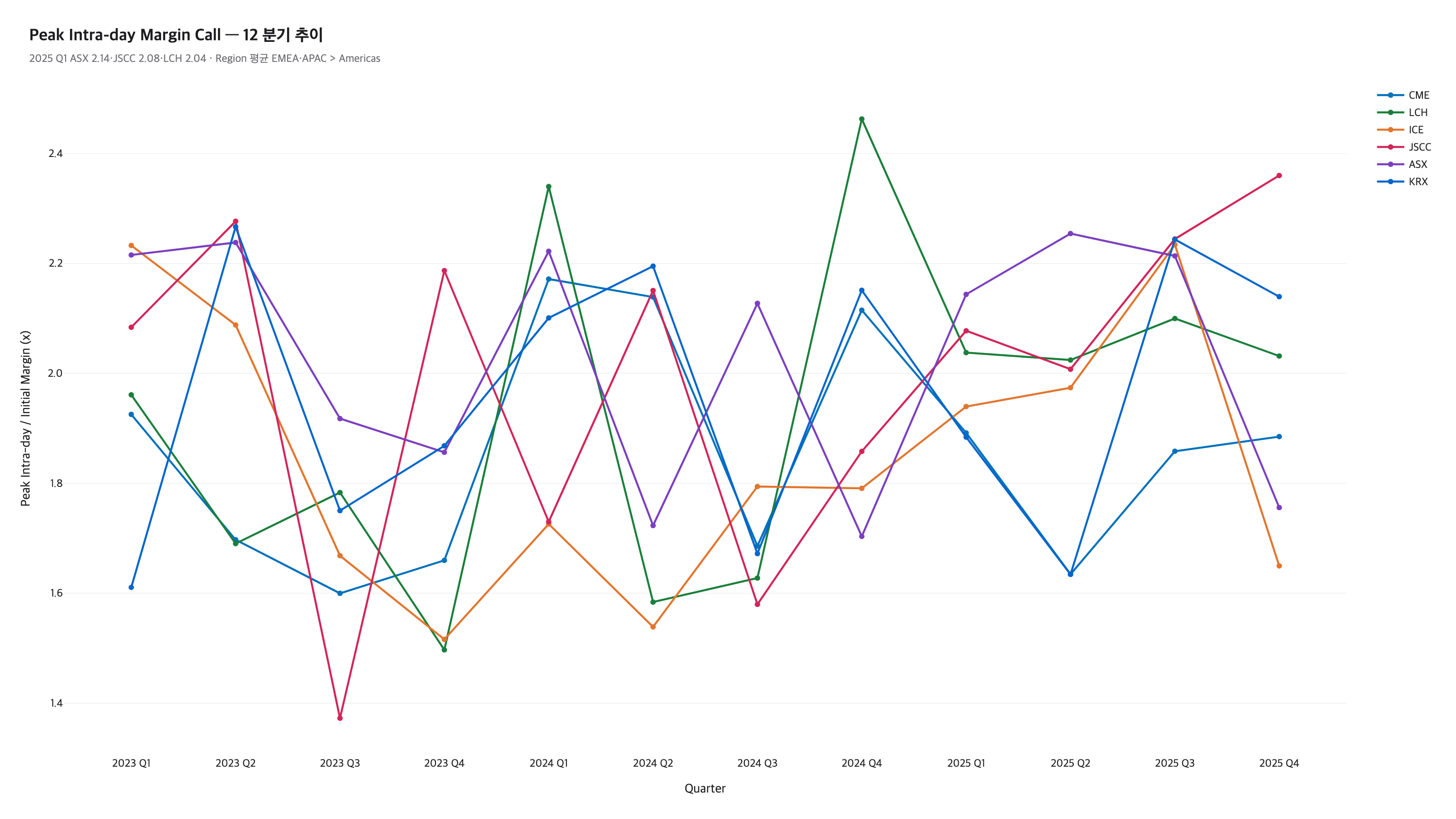

Peak Intra-day Margin Call trend (Ratio Timeline)

2025 Q1 ASX 2.14 · JSCC 2.08 · LCH 2.04 at the top. Region averages — EMEA 2.04 ≈ APAC 2.04 > Americas 1.92. Markets outside the US show larger intra-day spikes.

Member collateral: APAC · EMEA clearinghouses operate outside US close hours — a flow that first absorbs the volatility arising during Asian and European business hours is visible (for KRX, after-hours / night sessions were introduced by product: Options in 2010, Mini-KOSPI 200 Futures in 2016, KOSPI 200 Futures in 2021). For member firms with large FX and overseas-asset exposure, it can serve as a reference when timing how to communicate how the frequency and size of intra-day margin calls move quarter to quarter.

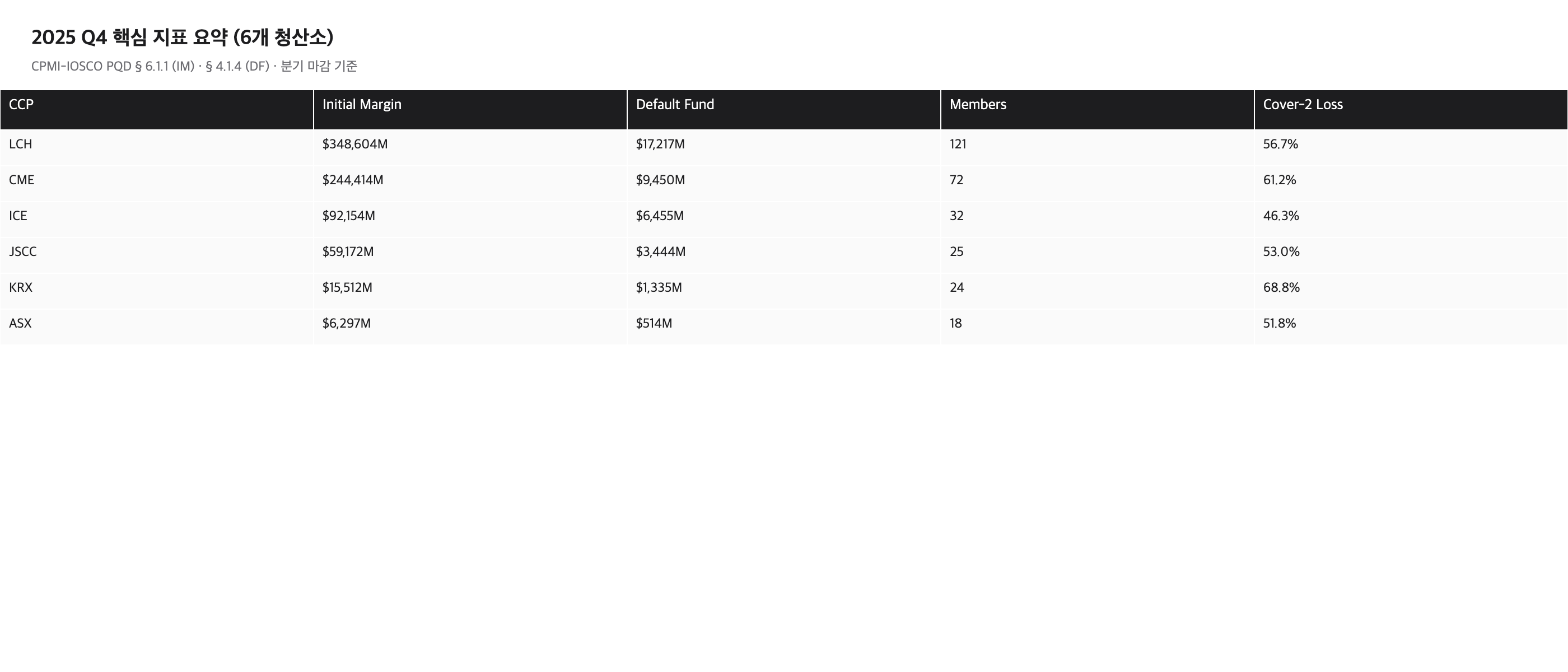

2025 Q4 core metrics summary (KPI Cards)

A one-screen summary for quarterly reporting. A consolidated comparison of size · Default Fund · Members · Cover-2.

Executive reporting: In board reporting material, a single slide can show KRX's position within the global benchmark. It is the screen format operators check first when opening a quarterly review meeting.